Whereas EU climate policies try actively to transform the European economy to make it more sustainable, the CSPP merely reproduces the current state of the corporate bond market. The ECB therefore mirrors investment choices made by financial markets, even though financial markets seem misaligned with a mitigation path limiting the global warming to 1,5°.

Download the Policy Note

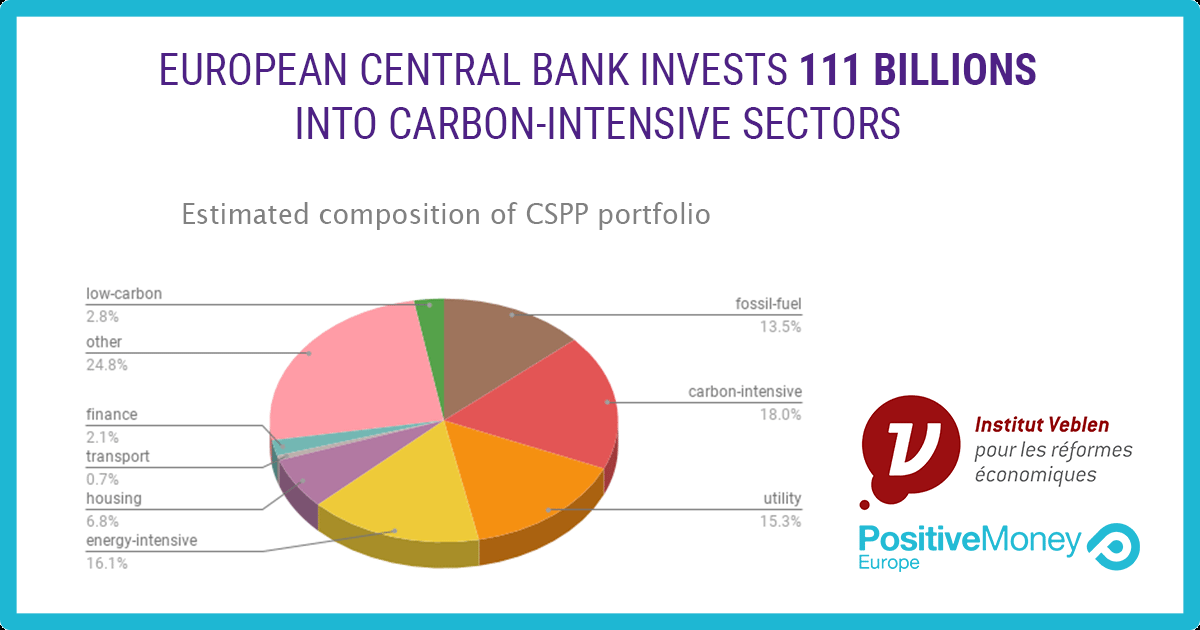

The weight of the most carbon intensive sectors within the CSPP portfolio is in line with the market neutrality principle claimed by the ECB, yet is profoundly troubling from the point of view of the ecological transition, as it maintains low capital costs and easy debt issuance conditions for the most polluting companies, without any assurance that these financial conditions serve the purpose of adjusting the underlying business and industrial models.

Download the Summary

This policy note suggests a way to integrate carbon emissions as a criterion in its own right, shaping central banks’ investment decisions and the collateral framework used for refinancing purposes. As the ECB intends to maintain its balance sheet volume at its current level even after the Quantitative Easing officially ends, the most urgent decisions concern the reinvestment of revenues from programs such as the CSPP. We consider that the technical difficulties related to estimating carbon emissions for different financial assets are real but surmountable and should not justify inaction.

Note on methodology

This policy note draws upon results from a study conducted by two researchers specialized in climate-related financial risk exposure, Stefano Battiston (FINEXUS Center for Financial Networks and Sustainability at University of Zurich) and Irene Monasterolo (Vienna University of Economics and Business). The study estimated the CSPP portfolio exposition to economic sectors which are highly climate-relevant and seem most impacted by the EU climate policy. For the first time, the study produced an estimate of the exposure for national central banks members of the Eurosystem.

The study applies a methodology developed for estimating individual investor’s portfolios (Battiston et al. (2017) and Monasterolo et al. (2018), measuring the extent to which the portfolio is compatible with the climate mitigation path limiting the global warming to 2°.The methodology is discussed in a technical note available at the FINEXIS website.